?")

Introduction

Let’s take a hypothetical example and consider a company as property. The value of a property can be evaluated in many ways using its location, area, future revenue or whether the property is residential, agricultural or business. If we consider a residential property, one of the parameters to gauze the property value is how much rental income it can generate in the future. The property analogy based on future rental generation is similar to valuing a company as discounted cash flow i.e. it is based on how much cash company can generate in future.

Key Takeaway

- Discounted cash flow analysis helps in valuation of a company or equity based on company’s future cash flows.

- It relies on the assumption of terminal value, risk free rate and free cash flow projection.

To value a company, let’s imagine the company having a five-year life. Let’s consider that the company will generate 100 million each year for five years and windup after that. Does the value of the company will be 500 million?

The answer is no, because the inflation erodes the value to money; 100 million today is not worth the same as 100 million after one year or two. The actual value of the company will be less than 500 million. We can’t just add up the 100 million each because the 100 million today is not worth the same as in year one, year two and so on. The value of the hundred million will erode as much as the time will pass by.

A hundred million received in year one will be little more than 100 million received in two-year time; a 100 million received in year two will be little more than 100 million received in year three and so on. The reason is that if you get 100 million today you would be investing it in fixed deposit or buying a property in that case the value of money will increase. Money has a time value, the sooner you will get it, the more it will worth it.

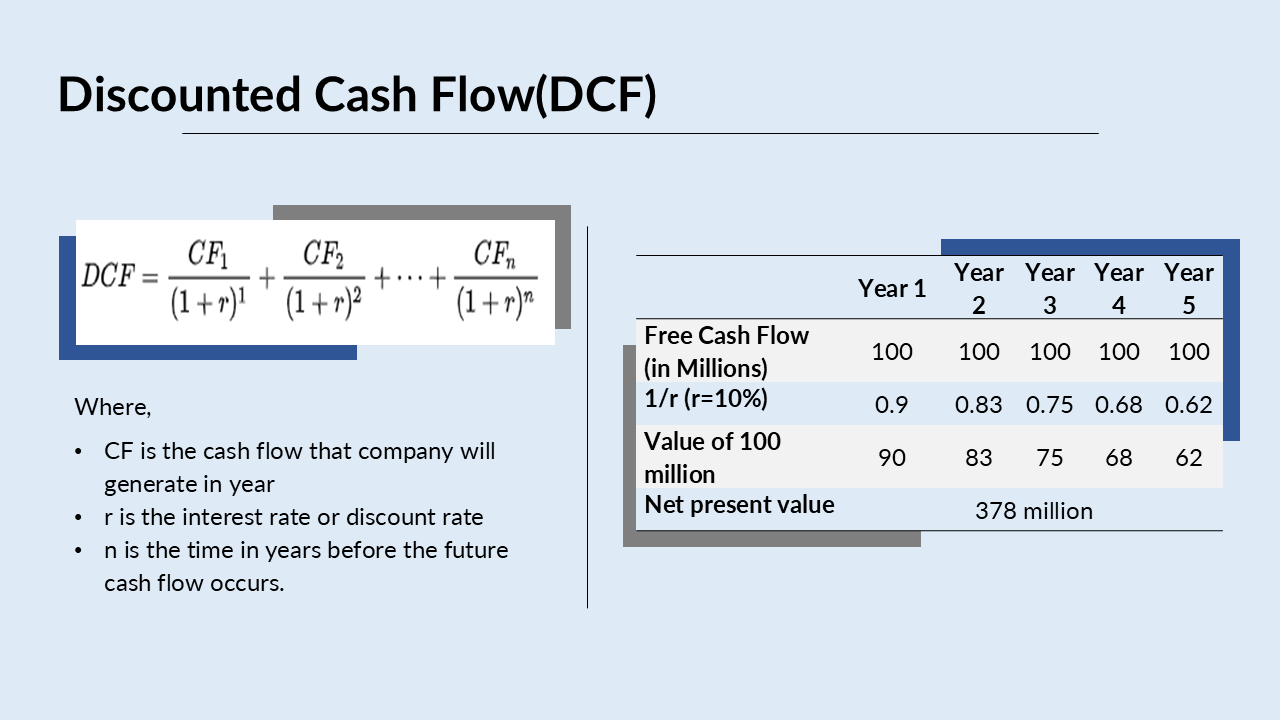

Let’s take another assumption, what is the risk-free rate that someone can get for 100 million invested, let’s consider it be 10%. If we get 10% return each year on 100 million and subsequently, we need to reduce the future money received in year one and so on to today’s money called discounting. We need to apply formula, to get the true value of money received in future in today’s value (given in the figure). So here r in the interest rate and n is the number of the period, here in our case r is 10% and n i.e. terminal value is five.

To calculate the true value, we apply the formula. We can see that in year one 100 million is worth only 90 million, in year two 100 million is worth 0.83, year three hundred million is worth 0.75, year four is 0.68 and year five is 0.62. We get this value by dividing 1/(1+r) to the power n to the 100 million. After summing the true values of 100 million for five years we get 378 million, not 500 million. So, a hundred million for five years is not worth 500 million but 378 million after five year.

Please note that the higher the interest rate are, the lower the value of 500 million in five-year time will be. If the company issue 100 million shares the share per value is 3.78 per share which is the true share price of a company. Using this method, we can predict the value of a share price today based on the future projection. We can also decide, whether the current share price reflect the true value, or is higher or lower than the value of the share.

Assumptions

- Just to clarify the assumption, the companies do not stop after five years. We can plug in the n value to get a reliable estimate to future value of a company. The terminal value could be based of assumption that after n number of years there is no point forecasting the future cash flow.

- The second assumption is that we forecasted the cash flow of 100 million each which is hard, if our assumption of forecast is wrong then the company value will change.

- The third assumption is the risk-free rate, the higher the risk-free rate the lower the value of the company will be. 10% reflect the number of things; the riskier the business is the higher the chances of going the risk-free rate higher.

Conclusion

Valuing a company is not easy, there is no full proof method. We can only predict it on the basis of assumption which can work like double edge sword. It required quite a bit assumption, it require forecasting, it require to come up with right interest rate, but it is recognized as good technique to value of the company or individual shares.